Don't Miss The World's #1 Executive Networking Event"

$27 Billion in Taxes, 70% Effective Rates: New Whitney Economics Report Puts a Price Tag on 280E’s Full Damage

Leading cannabis market data analyst Whitney Economics has released an updated analysis of how federal tax policy continues to shape the financial reality for state‑regulated cannabis operators. The refreshed report highlights the ongoing impact of IRS Code 280E, which prevents licensed businesses from taking most standard tax deductions and continues to drain cash from an industry already under pressure.

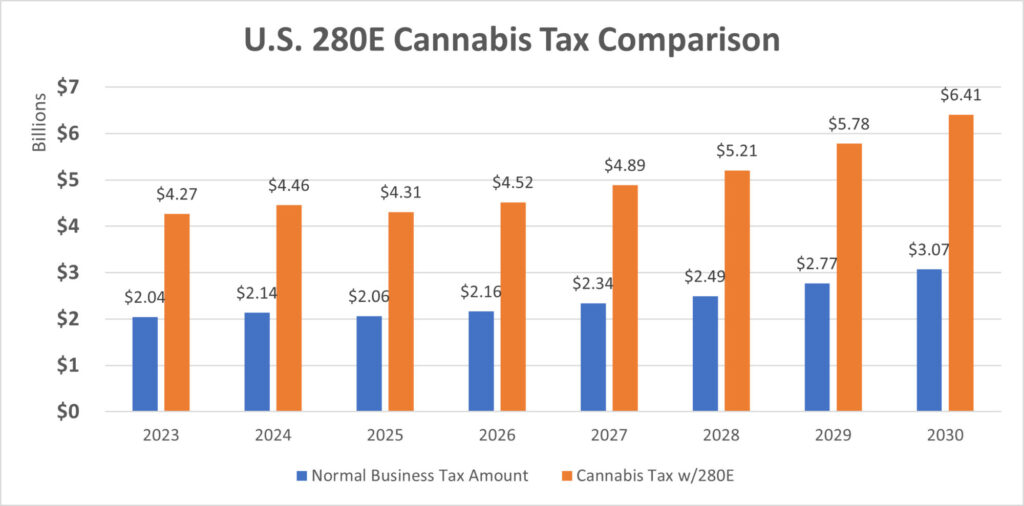

“The amount of additional taxes cannabis operators pay is staggering,” Whitney Economics chief economist Beau Whitney said in a statement about the new report. “In 2025, there was an estimated $2.24 billion in excess cannabis-related federal taxes due to the IRS’s 280E tax policy. The industry is being taxed out of business.”

Because cannabis remains a Schedule I substance under federal law, operators cannot deduct common expenses such as labor, legal fees, marketing, security, or banking. Whitney notes that the resulting effective tax rate can exceed 70% for some retailers. The policy was designed decades ago to punish illicit drug activity, but it has not been updated to reflect the modern state‑regulated cannabis economy.

If cannabis is rescheduled from Schedule I to Schedule III, operators would no longer be subject to 280E. Whitney says the change would immediately improve cash flow and profitability while boosting valuations and attracting new investment.

$27 Billion in Excess Taxes Since 2018

Since 2018, the industry has paid more than $27 billion in federal taxes, including $15 billion in excess 280E‑related taxes.

“With pricing compression occurring in every major U.S. cannabis market, tax revenues will no longer be the goose that laid the golden egg,” Whitney said. “In fact, declining state cannabis tax revenues are resulting in state cannabis tax increases, which will further hurt revenues, making the overall tax situation untenable for the industry.”

The lack of banking access compounds the strain. Whitney said the timing of federal reform remains uncertain.

“The timing of this reform, though, is still subject to significant speculation, especially with the change of the U.S. Attorney General,” he said. “We feel it is not a matter of if, but when this reform will occur.”

Even with the prospect of reform, Whitney cautions operators not to assume relief is imminent.

“We are advising operators in the industry to remain fiscally disciplined, despite the prospect of future reform,” he said. “Too many operators may be counting on this reform for their survival. They need to stay the course but be prepared to pivot quickly once the tax policy change occurs.”

280E Racks Up Operating Costs, Too

For operators, the headline tax numbers only capture part of the burden. James Stephens, CEO of Sinful, a leading cannabis brand in Montana, said the true cost of 280E is even higher.

“The $2.24 billion number is real, but it’s only the tax bill,” Stephens writes in an email to IgniteIt. “What nobody is quantifying is the cost of complying with 280E itself. Every cannabis operator in America is paying accountants and attorneys to perform structural and bookkeeping gymnastics just to survive the tax code.

“That overhead, the entity structuring, the [cost of goods sold] allocation strategies, the specialized tax counsel, adds a second layer of cost that doesn’t show up in Whitney’s numbers. 280E doesn’t just take your money. It forces you to spend more money figuring out how much it’s taking.”

Whitney’s updated analysis illustrates why 280E remains one of the most consequential federal policies affecting the legal cannabis economy. With operators facing sustained pricing pressure, rising state taxes, and limited access to financial services, the industry’s long‑term stability is increasingly tied to federal action. The report offers a clear reminder that meaningful tax reform is not simply a political debate. For many businesses, it is a prerequisite for survival.

AJ Herrington

April 13, 2026 • 4:31 pm